Many real estate investors are familiar with the benefits of using the traditional delayed 1031 exchange when selling investment property and purchasing like-kind replacement property. Investors have been taking advantage of this tax-deferred strategy for over one hundred years. Most of those exchanges occur in a traditional manner, where the relinquished property sells first, and the replacement property is purchased later.

Reverse Exchange

Occasionally, market conditions can present challenges for exchangers, especially when replacement property inventory is low, or when a particularly appealing investment property is available that must be closed prior to the sale of a relinquished property. In these instances, investors can use the lesser known (but very effective) reverse 1031 exchange to keep their transaction intact.

Advantages

A vital advantage of the reverse 1031 exchange is that it affords the seller additional time to find the right replacement property without settling for making a poor or rushed purchasing decision on an asset of lower quality or lower income potential within the traditional 1031 exchange 45-day identification window.

Another advantage of the reverse approach is that it can help save an exchange if the seller cannot close on the relinquished property. This can happen when the seller cannot get the asking price or when the buyer is unable to qualify for a loan, or for other reasons like failed inspections.

In either case, the seller can still identify and buy the preferred replacement property and is allowed up to six months to sell the existing property. That can alleviate a lot of pressure and anxiety, especially when the seller faces a significant tax obligation should the exchange fail.

Different Rules

Not surprisingly, different rules apply to a reverse exchange as compared to a traditional transaction. Reverse 1031 exchanges are more complex, and that is why it is essential sellers work closely with an experienced Qualified Intermediary, financial professional, and tax advisor when considering this option. Here are a few essential facts to know:

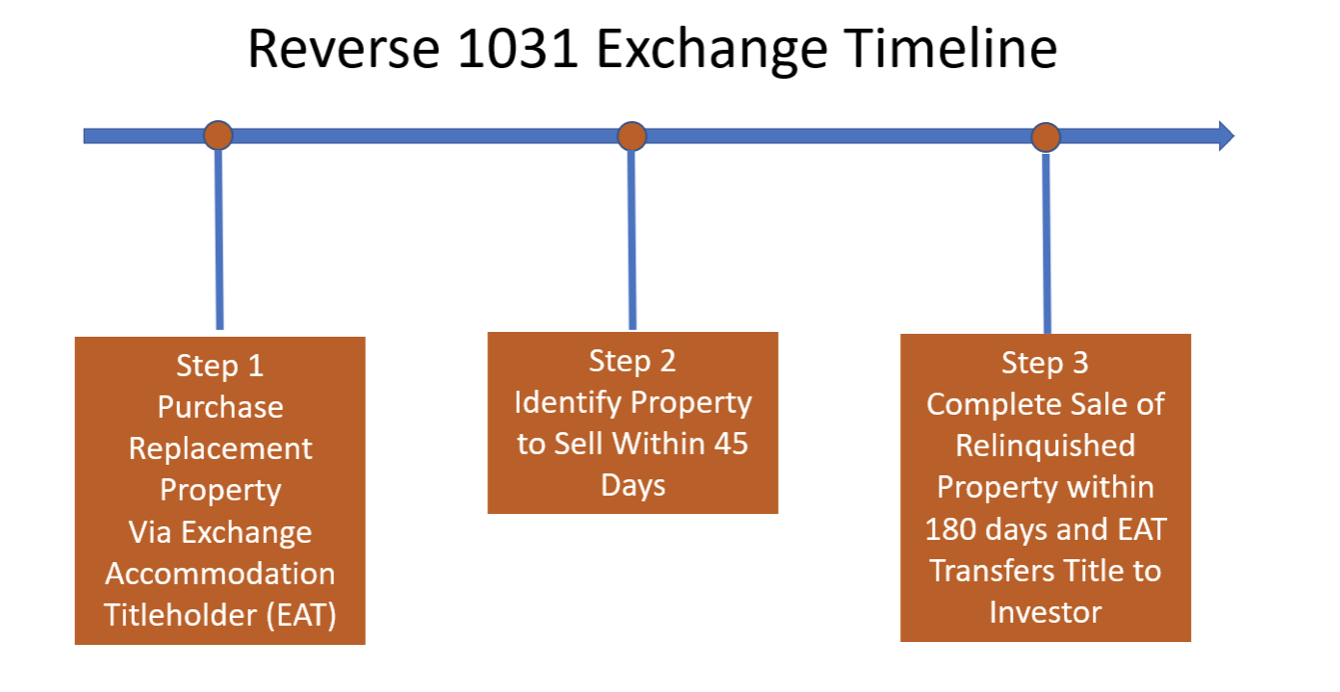

- The seller will need to acquire the replacement property via an intermediary called an Exchange Accommodation Titleholder (EAT) because IRS rules will not allow the seller to hold the title of both the un-relinquished property and the replacement property at the same time. The EAT is a single-purpose LLC created to hold and park title of the desired replacement property throughout the exchange process. The EAT is typically created by entering into a special qualified exchange accommodation agreement between the seller and a Qualified Intermediary (or affiliate) who manages the EAT.

- Deadlines for a reverse exchange are the same as for a delayed exchange but in reverse. The seller needs to Identify the relinquished property within 45 days of the EAT acquiring title on the replacement property. Then, the seller needs to Identify a buyer for the relinquished property within 180 days of when the replacement property was purchased.

Risks and Considerations

While a reverse 1031 exchange strategy can reduce the anxiety and risk of finding a replacement property, reverse 1031 exchanges are more complicated than delayed exchanges, requiring heightened awareness of the different requirements. There are potential disadvantages that should be considered, including:

- If the exchanger cannot sell the relinquished property within 180 days, they could lose the favorable tax treatment. As most real estate investors know, there is no certainty of when a property will sell and there is a risk that unexpected events can derail the acquisition process.

- The exchanger may need to reduce the price of their relinquished property to attract a buyer before the 180-day deadline.

- The exchanger must possess the financial ability to buy the replacement property before having received proceeds from the relinquished property. This can require a significant amount of free cash.

- If the seller cannot purchase the replacement property with cash, a loan may be required, and lenders may be reluctant to provide financing without the security of proceeds on the property to be sold. Interest costs may also be higher.

- Qualified Intermediary fees to complete a reverse 1031 exchange can be significantly higher relative to a tradition 1031 exchange.

If you consider a 1031 exchange for your investment property transaction and anticipate one or more of the potential challenges we discussed earlier, please contact us. We can help you determine if the “reverse” approach is the right one for you.

Help Save 1031 Exchanges.

Have you downloaded our latest Ebook?

Your Comments :