Investors considering the sale of a business property and looking to reinvest, may be familiar with Tenant in Common (TIC) property structure. Like a Delaware Statutory Trust (DST), both are securitized investments, and both qualify under the rules of a 1031 Exchange as defined by the IRS Code.

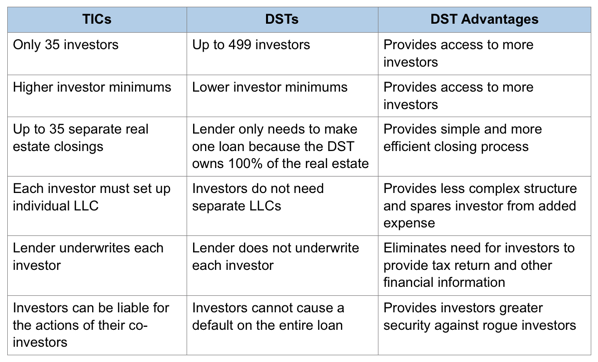

There was a time when the TIC investment structure fueled much of the rapid growth driving 1031 exchanges. That was a period between 2002 and 2007. TICs allowed up to 35 investors to pool funds and purchase larger institutional-class real estate.

Unfortunately, investor appetite for these investments became overheated, with many ultimately paying prices far above fair market value. Lenders contributed to this frothy environment with loose lending practices on over-priced assets.

When the Great Recession of 2008-2009 hit, the TIC structure was almost eliminated with many investors, lenders, and sponsors experiencing the pain of rent declines, cash flow shortfalls, mortgage defaults, and property value loss. During this stressful period, many TIC ownership groups also found it very challenging to gain the required unanimous approval required per most TIC operating agreements for approving property sales and new leases. The TIC structure as an investment vehicle for larger numbers of investors, with but a few exceptions, has now largely disappeared.

This created a void for investors still interested in diversifying their portfolios with a position in real estate. Enter the Delaware Statutory Trust, or DST, a specific type of trust structured to manage trust activities related to real estate assets.

DST’s retained a few of the common characteristics of TICs like:

- Both structures permitted fractional ownership of real estate with full 1031 Exchange tax deferral benefits

- Both structures also produced income that could be at least partially shielded through pass-through tax benefits

- Both types of investments were classified as securities and could only be offered and purchased through a licensed securities dealer or directly from the issuer

As a testimony to the concept of ‘needing something better’, DSTs were designed with numerous advantages over their ill-fated cousin and here are a few examples of how significantly the DST improved the investment structure:

Another major difference between TICs and DSTs is in the area of property loans. One of the most attractive aspects of the DST is that individual investors do not need to qualify for any property loans or have any recourse from the lender if the property fails. The trustee and/or the sponsor company bears full responsibility for any loan guarantees.

A TIC investment requires investors to submit financial statements to qualify as a borrower. While most TIC loans are non-recourse to the borrowers, TIC investors are, however, subject to certain penalties (bad boy carve-outs) if they engage in specified prohibited actions, such as filing for bankruptcy.

Due to all the mentioned issues associated with TIC structures, in general, lenders are no longer making loans to properties structured as TICs. This has led to almost a total shutdown of new investments in the TIC structure.

Fortunately, the new and improved DSTs have more than filled the gap of investor appetite for suitable 1031 exchange properties. The popularity of DSTs continues to increase every year.

Investors who may be considering DSTs should also be aware of certain limitations and trade-offs:

- All day-to-day property decisions including when to sell and lease properties are made by the DST sponsor/trustee. DST investors must be comfortable relying on a third party to manage their investment.

- DST interests may only be acquired by accredited investors having a net worth of $1 million or greater excluding their primary residence or annual income of $200,000 or greater if single or $300,000 or greater if married during the past two years with an expectation that the income will continue during the year the investment is made.

- There is no established secondary market for DSTs and investors should anticipate a 5 to 10-year period prior to being able to regain control of their invested equity. Although DST investors are free to sell their interests early to other accredited investors, the process can take weeks to months and the sale price is established based on what a buyer may be willing to pay at time of sale.

- DST investments are subject to various risks, including but not limited to the general risks related to investing in real estate, market risks and illiquidity, and returns are not guaranteed.

- Once formed, DSTs are not permitted to raise additional capital from their investors or obtain additional bank financing. In the event of cash shortfall, a DST sponsor has the option to convert the DST structure into an LLC structure (aka “springing LLC”) which would then allow them flexibility to seek additional capital. In a worse case, investors could be asked to invest additional funds and may also lose the ability to complete another 1031 Exchange if the sponsor is unable to restore the DST structure prior to sale or disposition of the property.

- Lastly, each DST has unique features including the track record of the sponsor, property type, location, cost structure, etc., that should be closely evaluated before an investment is made.

First Guardian Group has worked with thousands of real estate investors over our 17+ year history and can assist investors to make better informed decisions when considering DSTs or other types of real estate investments. Please contact us for more information.

Your Comments :