Those of you who have interacted with me over the years know that I generally favor a buy and hold strategy when investing in real estate. Provided that the economic fundamentals of a real estate investment remain sound, and there are no external factors that may necessitate selling, we found that our most successful clients rarely sell properties. They invest for the long term, avoid reacting to short term market changes, and count on time to be their friend.

However, investors need to be vigilant in spotting shifts in longer term fundamentals and consider reallocating investment funds if previous assumptions and investment strategies fail to deliver optimum results.

During the past year, we have seen a growing number of our clients selling investment properties they have held for long periods and reinvest proceeds in order to better position their real estate portfolios to better align with several strategic trends that are becoming apparent.

In this blog post, I would like to discuss the impact of three top factors that are driving our clients to consider reallocating real estate investment funds: Inflation, Recession, and Demographics.

Factor # 1: Inflation

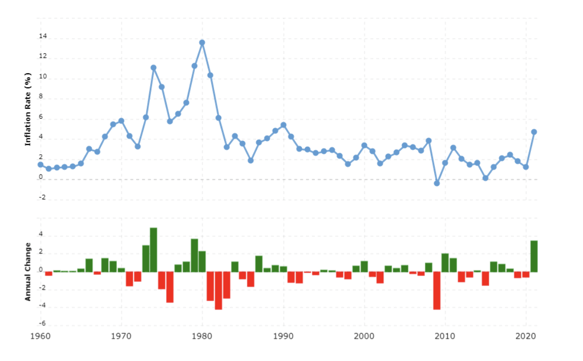

Notable economists have been signaling that higher rates of inflation may be with us for the foreseeable future. They cite underlying factors such as high government spending and monetary expansion during COVID, rising energy costs due to supply constraints, and higher borrowing costs due to rising interest rates. During most of the past 40 years, inflation has trended to range in an annual rate of 1% to 3%. For the past two years, the annual inflation rate has rapidly escalated and appear to be stabilizing at levels well above the historical Federal Reserve annual target of 2%.

Source: World Bank

This data is especially concerning to investors who are holding real estate assets with longer term leases that limit annual rent increases. Today, most leases of commercial office, industrial, and retail properties limit rent increases to less than 3% per year. If property income cannot keep pace with higher inflation rates, property values can be negatively impacted since sales values are highly correlated to the amount of income that a property is generating at the time of sale relative to comparable properties.

This realization has resulted in growing demand for more inflation resilient real estate assets having shorter term leases where rents can be more aggressively raised such as apartments, storage, student housing, and select senior housing properties.

While select non-residential and retail properties remain attractive to many investors, we have seen a decided shift in our investor base towards more inflation resilient assets.

Factor # 2: Recession

During the 70s and early 80s, the US experienced not only heightened inflation rates, but an extended low growth environment in the US that was called Stagflation. To curb persistent inflation, the Federal Reserve Chairman at the time, Paul Volker, took extraordinary steps to raise interest rates from 11.2% in 1979 to 21.5% in 1981 which helped trigger a significant recession from 1980 to 1982.

When learning real estate investing basics from my father. I remember his advice for investing in difficult economic periods.

“Paul, if I had two dollars to spend during the Great Depression, I would spend the first dollar to put food on the table and the second dollar to keep a roof over our head.”

In challenging economic times, people generally cut back on discretionary items and limit spending to necessities such as food, shelter, healthcare, etc. While asset values may decline during recessions, income will tend to hold-up since people will strive to pay for food, other necessities, and to maintain a place to live. As I have witnessed through the roughly 8 or so recessions that I have lived through, real estate assets that are regarded as necessities such as well positioned apartments, grocery and discount stores, and medical centers tend to perform better than commercial office and non-necessity retail.

Factor # 3: Demographics

Early in our real estate education process, we all learned these three most important keys to smart real estate investing:

Location, location, location

To which my father wisely added:

“Paul, invest in places that people are moving to and not away from.”

As I have previously written over the past 3 years, we have seen a tremendous population shift across the US that greatly accelerated during COVID which is being caused by the following factors”

- Work from home – a growing number of employers are not only permitting but encouraging remote work when practical. This is done not only to retain talent in today’s tight labor market, but to increase productivity since employees no longer need to give up potentially productive time to commute to work.

- Flight from more expensive, higher crime urban markets – as remote employment gains greater acceptance, younger workers are moving to areas offering lower living costs and lifestyles that may be preferable to living in large cities.

- Desire to raise a family – Millennials and Generation X, i.e., folks born between 1965 and 1996 that represent the largest group of our population who are starting and raising families. Many can no longer afford to live where they currently live and work and want to live in an area with good schools, low crime, and diverse employment opportunities. Large employers are recognizing this trend and are expanding their operations to such areas nationwide thereby creating new real estate investment opportunities.

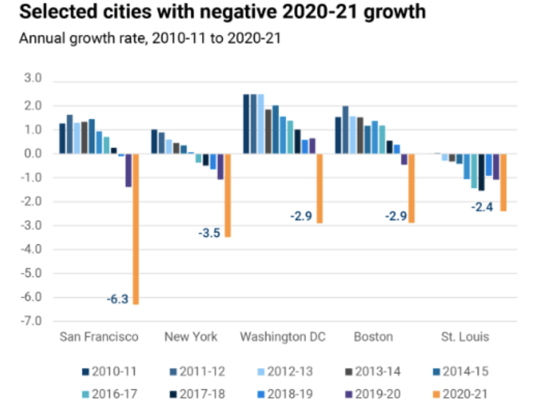

Here’s a recent snapshot of large cities who are losing population:

Source: Brookings Metro

Residents leaving these and other declining markets are generally moving to Sunbelt state locations with diverse employment opportunities including cities of Austin, Phoenix, Tampa, Denver, Huntsville, Raleigh-Durham, Charlotte, among many others. Housing options in these “go to” cities are limited since not enough new housing units are being built to meet demand. Rising interest rates are also making it more difficult to purchase and thereby creating more demand for apartments in attractive submarkets.

This trend does not show signs of slowing and is being exploited by a growing number of our clients who, for example, are selling rental properties in California and redeploying their equity in communities that are posed to long-term growth.

Summary

To manage inflation and recession risk and take advantage of more attractive new investment markets, investors should consider reallocating their real estate assets to different investment classes and locations.

This may be an excellent time for you to consider reallocating real estate investment to help manage inflation and recession risks while still aiming for attractive overall returns.

Please contact us at info@firstguardiangroup.com for assistance to analyze your current real estate investments and to learn more about reinvestment options that may better your long-term investment goals. You can also schedule a meeting with me here.

2 Longer term Triple Net Leases (NNN) do place a burden on tenants to cover rising costs of building operation and maintenance thereby providing a degree of inflation protection.

Your Comments :